$SKHY has the cleanest current exposure to the memory segment where $NVDA roadmap is creating the most value.

If HBM content per AI rack climbs from the low hundreds of thousands today to potentially more than $1M with Rubin Ultra then SK Hynix becomes a direct bet on structural

$SKHY $MU and a multi year run ahead for memory. Constraints will last beyond the end of the decade. Big day for SK Hynix. 👀

SK Hynix is the global HBM leader with direct exposure to $NVDA and the most supply constrained corner of the AI memory stack. So why does it still trade at a discount to $MU?

A cleaner US listing could close that gap fast. New Earnings Edge 👇

What to watch for when SK Hynix lists today:

If you want to hear Daniel and Shay discuss this in depth, go watch our most recent episode of The Futurum Equities Podcast linked below...

The AI Bubble Bears want this cycle to be like cycles of the past. And they will mock the whole “this cycle is different” talking point. But I’m just going to say it.

This cycle is different. 🚀

$10+ Trillion in cumulative capex by 2030

Memory supply and demand won’t find parity until 2030 (or later) and with new AI powered innovation in and out of the datacenter the constraint will remain giving memory names asymmetric pricing power for a prolonged cycle that is still at its beginning.

$SOXX Every dip gets bought. Because those that see what is happening with AI know it is still very early. 💪🏻📈

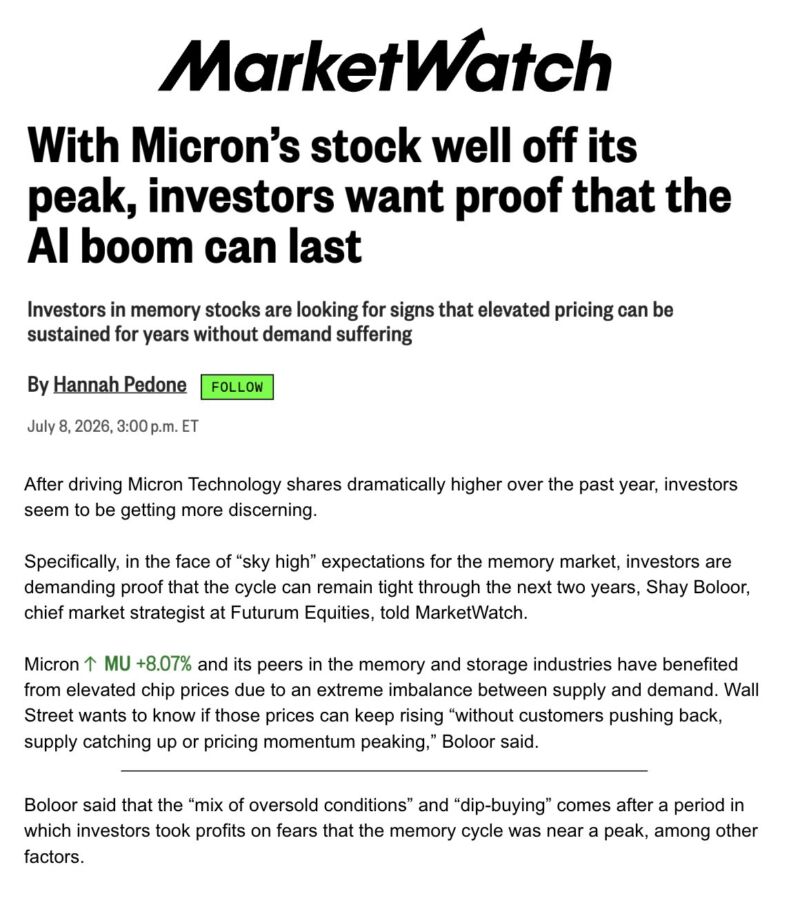

Great to be featured on MarketWatch discussing the recent $MU drawdown.

I think the expectations got extremely high after a massive move and the market now wants proof that the memory cycle can stay tight through 2027 and 2028 without customer pushback or pricing momentum

$CBRS targets 200MW of AI compute across Europe by late 2027, betting on demand for non-Nvidia silicon solutions.

The build-out reflects growing enterprise and cloud provider interest in diversified AI compute options beyond GPUs.